The financial world has become more accessible to citizens and is no longer an exclusive topic for experts. Moreover, changes in economic culture due to crises and globalization require people to understand how finances work and how to manage them.

Issues such as credit, savings, debts, pensions, taxes, and even entrepreneurship are relevant in the daily life of the population in any country. Therefore, Financial Education is crucial to making informed personal and social decisions. It is not merely a matter of knowing about the products and services of banking institutions but of examining consumption patterns, developing a critical perspective of credit advertising, measuring the impact of economics on socio-emotional issues, and, generally, making financial choices that support holistic well-being.

OCDE defines financial literacy as “knowledge and understanding of financial concepts and risks, as well as the skills and attitudes to apply such knowledge and understanding in order to make effective decisions across a range of financial contexts, to improve the financial well-being of individuals and society, and to enable participation in economic life.”

The Program for International Student Assessment (PISA) of the OECD (2022) analyzed the financial literacy of 15-year-olds from a representative sample of 23 nations. It established that 11% of the world’s population was at level 5, that is, a capacity to evaluate and interpret a broad panorama of complex financial products and problems and the implications of income and investment taxes. However, 18% performed at or below level 1, representing the ability to recognize the difference between needs and wants, make easy decisions about day-to-day expenses, and understand the purpose of basic documents such as an invoice.

Moreover, the PISA 2022 data showed that 63% of students already had a bank account, 62% had a debit card, and many had already shopped online. They also exhibited positive financial behaviors, such as saving, comparing prices, and avoiding the influence of friends on spending decisions, which are indicators of a higher level of financial literacy.

It should be noted that the study sample brought together students from different socioeconomic and family backgrounds. It was found that more men than women claimed to be exposed to monetary issues in their daily lives at home and school, even discussing news of this nature with their parents. On the other hand, students in a more disadvantaged socioeconomic context had fewer opportunities to learn about financial topics.

In short, the research suggests that financial literacy is not limited only to those with large sums of money to invest but is relevant to everyone, especially those on tight budgets with little margin for error in economic decisions.

Inclusion in the financial system from an early age can contribute to successful citizens who are competent with mortgages and even cryptocurrencies. Given this paradigm, Financial Education must be integrated into curricula at all academic levels and lifelong learning programs.

An integral part of the curriculum

Financial literacy enables students to navigate opportunities and challenges in this area in real life, which helps reduce unemployment. Similarly, it contributes to producing informed and aware citizens with a sense of social responsibility, understanding that their financial decisions impact their lives and the collective well-being of their community.

For her part, the Ecuadorian educator and Minister of Education, Alegría Crespo Cordovez, emphasizes that people are exposed to money daily; it is connected to their needs, personality, and the ability to manage emotions and control impulses. So, like any relationship, this bond requires care and boundary-setting to balance giving and receiving.

“Promoting the understanding of concepts about savings, debts, investments, taxes, and policies, among others, can ensure proper management of personal finances and allows for the training of entrepreneurs and innovators who can make decisions about their financial growth and economic security. […] If we want to strengthen micro-entrepreneurs and producers, we must introduce curricular training in Financial Education beginning in early childhood, with pedagogical resources adapted to children’s ages and school cycles because the knowledge acquired at this stage is central to the advancement of their intellectual skills and the configuration of their thinking,” she says.

Establishing a comprehensive approach to people’s holistic development, encompassing cognitive, emotional, social, physical, and ethical aspects, is essential. It recognizes students’ diverse needs and abilities while preparing them for an ever-changing professional landscape. She adds that teaching financial concepts and promoting values and skills leads to responsible decision-making.

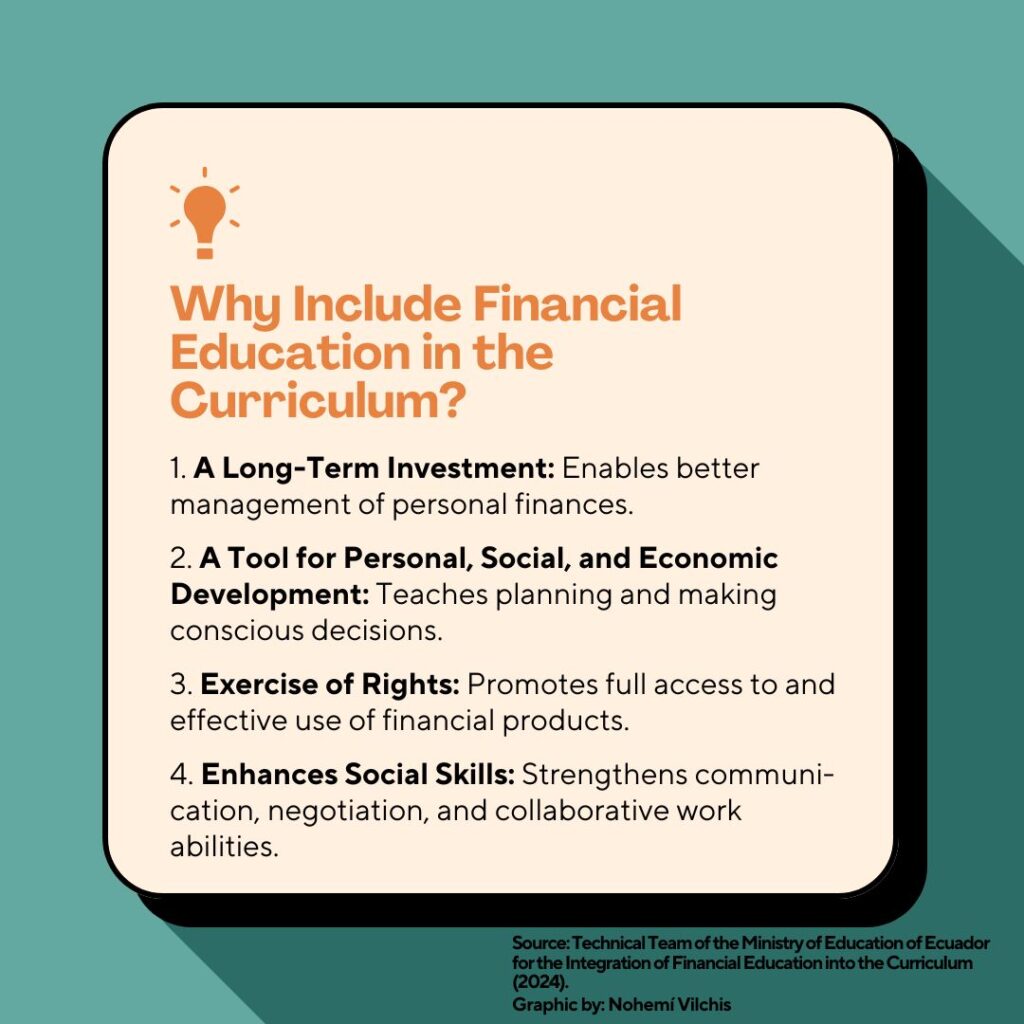

In summary, the Technical Team for the Curricular Insertion of Financial Education in the Ministry of Education of Ecuador points to four benefits of adding financial content and skills to the school curriculum:

- A long-term investment: students who better understand how to manage their personal finances will have greater possibilities for credit, savings, and investments and, above all, can avoid indebtedness in adulthood and throughout their lives.

- Tool for personal, social, and economic development: promotes citizens’ autonomy while reducing poverty and the inequality gap, improving the population’s economic situation by teaching them to plan and make conscious choices.

- Full exercise of rights: assists in familiarizing citizens with the responsibilities associated with accessing and using financial products and examining that information with objective data and evidence.

- Social skills: enhances communication, the ability to negotiate, and collaborative work in financial environments, promoting effective interaction and better coordination in decision-making.

Talking about money is usually taboo in many cultures. However, financial literacy helps break down the stigma and fear of dealing with the unknown. According to Tomas Hergott, a specialist in finance, investment instruments and services are produced when an educational process is persistent, transparent, sophisticated, and accessible. Under such conditions, people better conceptualize the fundamentals of risk and value in investments, such as the inverse relationship between risk and return, the investment currency, or the asset issuers’ geographical location.

Since its inception, Financial Education has evolved from managing the home to becoming a fundamental step in formal education. The latter did not occur until the 90s when different countries integrated this type of program into their school curricula. This approach became even more relevant after the 2008 financial crisis, spotlighting many people’s limited general financial knowledge and the economic consequences of financial illiteracy.

Nowadays, Financial Education covers a wide range of topics, from saving to planning for retirement. There are even resources that facilitate financial learning, for example:

- Games like Monopoly and Cashflow provide some exposure to financial concepts while students learn playfully.

- Simulation tools, such as those that emulate the stock market, make “investing” possible without being a real risk.

- Mobile applications like Mint and YNAB are used for efficient budgeting and managing personal finances.

- Educational platforms, like Khan Academy, provide free courses on financial topics.

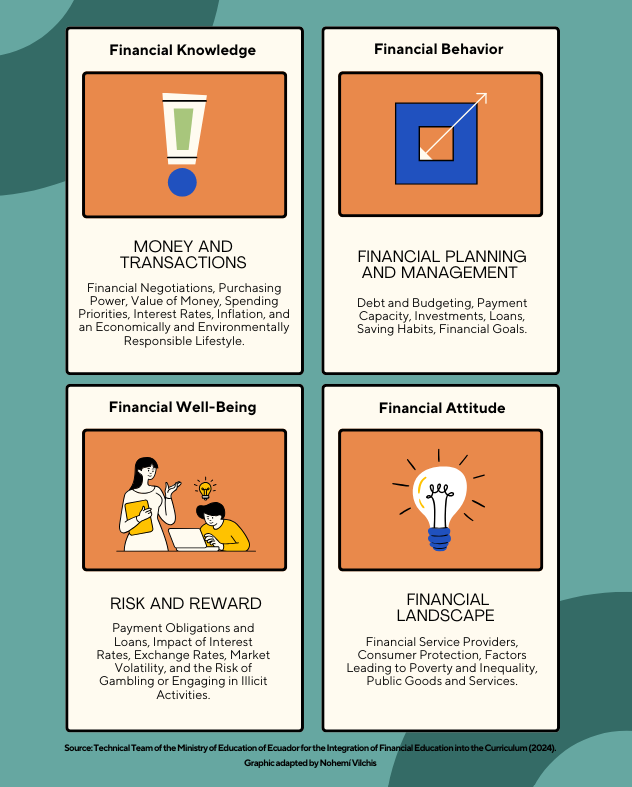

However, the Technical Team for the Curricular Insertion of Financial Education in the Ministry of Education of Ecuador proposes a specific path suggesting the adoption of a series of dimensions:

Also, they recommend that the insertion process in the curriculum must be adjusted to particular educational contexts and cover stages of planning, design, implementation, and subsequent monitoring and evaluation of its effectiveness. Moreover, their path contemplates the interdisciplinary collaboration of educational authorities, teachers, students, family members, and community actors. However, the cooperation of academic institutions, governments, non-governmental organizations, and the private sector also contributes to creating satisfactory educational policies, effective programs, and teacher training.

Insertion in different countries

By reference, it is relevant to mention the world context, where Financial Education is recognized as crucial in lifelong learning. Students in the United States, Canada, and the United Kingdom must complete courses in this subject before graduating from high school. Canada made this a primary approach in the social studies curriculum.

One study between Germany and the United States showed that, although both countries improved their students’ financial knowledge, the cognitive structure of the knowledge acquired differed significantly, underscoring the need for educational approaches tailored to local contexts.

Meanwhile, in Finland, the gamified program Yrityskylä improved students’ financial knowledge, and in Indonesia, integrating Financial Education into business training increased students’ competition, better preparing them for entrepreneurship.

Sweden, in turn, adopted this approach in social studies to understand finance and its connection to socioeconomic structures. Nevertheless, it has also permeated the traditional approach to managing money. Malaysia has used video clips as a pedagogical tool to identify the financial elements of daily life there.

In Spain, the Basic Scale of Entrepreneurial Competencies (BSEC) accurately evaluated and measured financial entrepreneurial skills acquired in a high school education. In 2021, the National Securities Market Commission (CNMV), the Bank of Spain, and the Ministry of Economic Affairs and Digital Transformation proposed a plan for the school curriculum for all educational levels. This included a gamification strategy at an early age, using applications like Life Hub, Goalsetter, or Banqer to identify concepts of good financial health. Additionally, crucial financial sector morals were obtained through workshops and stories.

Their plan stemmed from a complaint that 15% of students do not surpass the basic level of achievement in financial skills. Therefore, these organizations projected the inclusion of issues related to controlling money in primary education, credit and savings, and basic security measures for online purchases, passwords, and data protection.

Meanwhile, Financial Education has been more notable in Mexico in recent years. However, despite initiatives by government and financial institutions to promote this vision in schools, much work remains to be done to ensure quality education. For example, it has been observed that programs positively impacting financial literacy require continuous review and adaptation to ensure their effectiveness.

In addition, the 2015 National Financial Inclusion Survey (ENIF), carried out by the National Banking and Securities Commission (CNBV), resolved that 52.9% of the population has no accounts in financial institutions, only 47.5% has informal savings, and 21.5% never save. The most concerning issue is that Banamex Mexico and the National Autonomous University of Mexico (UNAM) determined that many citizens (50%) do not receive enough income to save. If they do, they do not know what to invest in, so they set up a business.

Globally, only 33% of adults have adequate financial education. This figure rises to 67% and 68% in the United Kingdom and Canada, but 32% in Mexico. Similarly, recent comparative research on a global scale revealed that levels of financial literacy are low from Peru to Italy and Singapore to Japan, whose citizens lack the notions required for full development.

In Latin America, adoption has variations. Brazil and Chile have integrated this approach into their education systems. Still, some other countries in the region face challenges like a lack of resources and teacher training to achieve efficient integration.

According to Santiago David Muñoz Solórzano of the Pontificia Universidad Católica del Ecuador, an analysis of literature and empirical research highlighted progress in the inclusion of financial content but also referred to underlying challenges like those mentioned above in the region and insufficient institutional support for teaching this subject in schools.

“Being financially educated allows you to be aware of the decisions that impact the different stages of life,” pointed out Alejandro Mungaraya, Nidia Gonzalez, and Germán Osorio.

As Víctor González, Intrum’s Director of Brand & Communications in Spain, explains, what is known about personal finance has been learned based on experience and, on multiple occasions, by bad economic decisions of our own or third parties. Therefore, escalating learning in financial matters is essential for groups that lack financial knowledge and to equalize opportunities for all.

Individuals do not need to become financial experts, but it is fundamental to provide them with training that enables them to select suitable financial advisors or tools that support them in making assertive choices.

The Curriculum and Evaluation Unit (UCE) of the Ministry of Education of Chile made beneficial support materials that fortify personal financial culture available to the public. Within its sections, one can find suggested readings for a healthy financial life, financial planning resources, and even a list of frequently asked questions that could be embarrassing for being so “basic,” but they are commonly asked.

The deficiency of financial literacy in the younger generations is concerning, as they constitute a substantial portion of the labor market. Their insufficient financial knowledge hampers their potential and overall development. It is imperative to incorporate financial education from an early age, as these individuals will eventually become university students and professionals responsible for making pivotal business decisions. Early exposure to relevant courses or materials during their academic journey will better equip them to achieve holistic well-being throughout both their professional and personal lives.

What resources or strategies would you implement in your teaching work, or what tools would you add to optimize the management of your personal finances?

Translation by: Daniel Wetta